Why Italy's inheritance taxes aren't as high as you might expect

Published: 24 Jul, 2020 CET.

Updated: Fri 24 Jul 2020 11:48 CET

Inheritance taxation in Italy is much more advantageous than in other European countries. In fact, it ranges from 4% to 8% - and in many cases is not even applicable. But what exactly is the inheritance tax and how does it work in Italy? Tuscany-based tax experts MGI Vannucci e Associati explain.

Inheritance tax must be paid by residents in Italy under certain conditions, that will be described below, when they inherit property - both real estate and movable property - wherever this heritage may be located (therefore also on assets held abroad).

The Italian inheritance tax concerns not only the assets of Italian citizens, but also all assets, in Italy and abroad, of foreign citizens if they have their tax residency in Italy at the time of their death.

On the other hand, the Italian inheritance tax is calculated only on assets located in Italy if the deceased, whatever their citizenship, is not a tax resident in Italy at the time of their death.

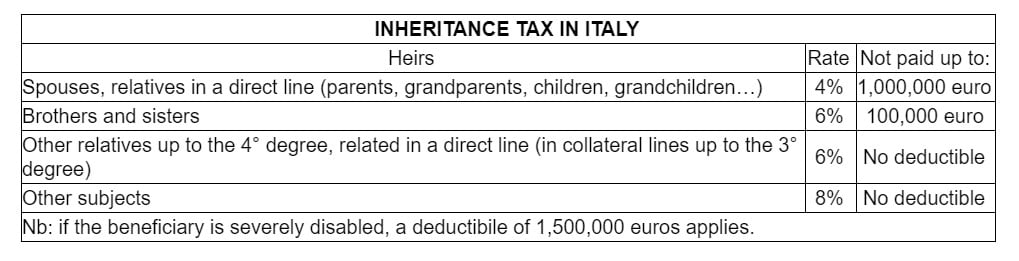

The Italian law governing inheritance tax provides for different taxation depending on who is receiving the inheritance, and there are some cases in which no tax is due.

In particular:

-

If the heirs are the spouse, children, or other relatives in a direct line (father, mother, grandchildren), a one million euro deductible is provided for each heir under which no tax is due; 4% tax is due on the part exceeding one million euros;

-

If the heirs are brothers or sisters, there is a 100,000 euro deductible under which no tax is due; a tax of 6% is due on the part exceeding 100,000 euros;

-

If the heirs are relatives other than those indicated above, there is no limit on taxation up to the fourth degree of relationship, and the inheritance received is taxed at 6%;

-

For all the other heirs, there is no limit on the taxation and the inheritance received is taxed at 8%

-

Furthermore, if the heir is a disabled person, the deductible under which no tax is due rises to 1.5 million euros.

For example, assuming that an Italian resident with a patrimony of four million euros dies, leaving his wife and two children as his heirs, with the patrimony shared equally among them, the following taxation occurs:

Each heir receives a fortune of 1.33 million euros (1/3 of 4 million). Since the heirs are the spouse and the two children, the exemption allowance of one million euros applies to each of them, and 4% is applied to the surplus. So each has to pay 13,333 Euros (4% of 333,333 euros).

Therefore, on a total inheritance of 4 million, the inheritance tax to be paid is equal to 40,000 euros (with an incidence of only 1% on the total inherited assets).

The following table offers a summary:

If real estate located in Italy is included among the assets to be inherited, the mortgage tax of 2% and the cadastral tax of 1% is due, without any benefit from deductible exemptions.

Therefore, in the event that real estate located in Italy is inherited, there is still a 3% tax burden to be applied. This is, however, on the cadastral value of the asset, which currently in Italy is generally much lower than the market value.

If real estate located in Italy is included among the assets to be inherited, the mortgage tax of 2% and the cadastral tax of 1% is due, without any benefit from deductible exemptions.

Therefore, in the event that real estate located in Italy is inherited, there is still a 3% tax burden to be applied. This is, however, on the cadastral value of the asset, which currently in Italy is generally much lower than the market value.

Photo: AFP

As we have already said, in cases where the inheritance tax is due in Italy, the assets held in foreign countries must also be calculated.

In this case, it is probable that, for assets located abroad, an inheritance taxation will most likely also apply in the country in which these assets are located. In this case there is thus the risk that a hypothesis of double taxation is generated.

According to Italian legislation, where inheritance tax has been applied to the same asset abroad, said foreign tax can be deducted from the tax to be paid in Italy.

In addition, Italy has signed bilateral agreements aimed at eliminating double taxation in matters of succession with the following countries: Denmark, France, the United Kingdom, Greece, Israel, the United States of America, and Sweden.

READ ALSO:

Photo: AFP

As we have already said, in cases where the inheritance tax is due in Italy, the assets held in foreign countries must also be calculated.

In this case, it is probable that, for assets located abroad, an inheritance taxation will most likely also apply in the country in which these assets are located. In this case there is thus the risk that a hypothesis of double taxation is generated.

According to Italian legislation, where inheritance tax has been applied to the same asset abroad, said foreign tax can be deducted from the tax to be paid in Italy.

In addition, Italy has signed bilateral agreements aimed at eliminating double taxation in matters of succession with the following countries: Denmark, France, the United Kingdom, Greece, Israel, the United States of America, and Sweden.

READ ALSO:

-

Why moving to southern Italy with a foreign pension could cut your tax bill

-

The little-known tax rule that's got the super-rich flocking to Italy

Finally, we should draw attention to the fact that, in the presence of assets worth more than 100,000 euros, or in any case in the presence of properties (whatever the value) that have fallen into succession in Italy, a specific declaration of succession must be presented. It is advisable to contact specialized professionals for this requirement.

Taxation on inheritance in Italy is certainly very "generous" compared to what happens in other countries.

For this reason, for some years now there have been discussions in Italy of revising this tax, providing for an increase. In this sense, legislative proposals have been promoted aimed at increasing the rates and reducing the exemptions on succession tax.

At the moment, however, the taxation applicable to successions in Italy is as described in this article.

MGI Vannucci e Associati are a team of English-speaking chartered accountants and tax experts based in Tuscany, Italy.

READ ALSO: The real cost of buying a house in Italy as a foreigner

Comments

See Also

Inheritance tax must be paid by residents in Italy under certain conditions, that will be described below, when they inherit property - both real estate and movable property - wherever this heritage may be located (therefore also on assets held abroad).

The Italian inheritance tax concerns not only the assets of Italian citizens, but also all assets, in Italy and abroad, of foreign citizens if they have their tax residency in Italy at the time of their death.

On the other hand, the Italian inheritance tax is calculated only on assets located in Italy if the deceased, whatever their citizenship, is not a tax resident in Italy at the time of their death.

The Italian law governing inheritance tax provides for different taxation depending on who is receiving the inheritance, and there are some cases in which no tax is due.

In particular:

- If the heirs are the spouse, children, or other relatives in a direct line (father, mother, grandchildren), a one million euro deductible is provided for each heir under which no tax is due; 4% tax is due on the part exceeding one million euros;

- If the heirs are brothers or sisters, there is a 100,000 euro deductible under which no tax is due; a tax of 6% is due on the part exceeding 100,000 euros;

- If the heirs are relatives other than those indicated above, there is no limit on taxation up to the fourth degree of relationship, and the inheritance received is taxed at 6%;

- For all the other heirs, there is no limit on the taxation and the inheritance received is taxed at 8%

- Furthermore, if the heir is a disabled person, the deductible under which no tax is due rises to 1.5 million euros.

For example, assuming that an Italian resident with a patrimony of four million euros dies, leaving his wife and two children as his heirs, with the patrimony shared equally among them, the following taxation occurs:

Each heir receives a fortune of 1.33 million euros (1/3 of 4 million). Since the heirs are the spouse and the two children, the exemption allowance of one million euros applies to each of them, and 4% is applied to the surplus. So each has to pay 13,333 Euros (4% of 333,333 euros).

Therefore, on a total inheritance of 4 million, the inheritance tax to be paid is equal to 40,000 euros (with an incidence of only 1% on the total inherited assets).

The following table offers a summary:

If real estate located in Italy is included among the assets to be inherited, the mortgage tax of 2% and the cadastral tax of 1% is due, without any benefit from deductible exemptions.

Therefore, in the event that real estate located in Italy is inherited, there is still a 3% tax burden to be applied. This is, however, on the cadastral value of the asset, which currently in Italy is generally much lower than the market value.

Photo: AFP

As we have already said, in cases where the inheritance tax is due in Italy, the assets held in foreign countries must also be calculated.

In this case, it is probable that, for assets located abroad, an inheritance taxation will most likely also apply in the country in which these assets are located. In this case there is thus the risk that a hypothesis of double taxation is generated.

According to Italian legislation, where inheritance tax has been applied to the same asset abroad, said foreign tax can be deducted from the tax to be paid in Italy.

In addition, Italy has signed bilateral agreements aimed at eliminating double taxation in matters of succession with the following countries: Denmark, France, the United Kingdom, Greece, Israel, the United States of America, and Sweden.

READ ALSO:

- Why moving to southern Italy with a foreign pension could cut your tax bill

- The little-known tax rule that's got the super-rich flocking to Italy

Finally, we should draw attention to the fact that, in the presence of assets worth more than 100,000 euros, or in any case in the presence of properties (whatever the value) that have fallen into succession in Italy, a specific declaration of succession must be presented. It is advisable to contact specialized professionals for this requirement.

Taxation on inheritance in Italy is certainly very "generous" compared to what happens in other countries.

For this reason, for some years now there have been discussions in Italy of revising this tax, providing for an increase. In this sense, legislative proposals have been promoted aimed at increasing the rates and reducing the exemptions on succession tax.

At the moment, however, the taxation applicable to successions in Italy is as described in this article.

MGI Vannucci e Associati are a team of English-speaking chartered accountants and tax experts based in Tuscany, Italy.

READ ALSO: The real cost of buying a house in Italy as a foreigner

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.